TTC Video - How to Plan for the Perfect Retirement

TTC Video - How to Plan for the Perfect Retirement

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 5h 57m | 5 GB

Lecturer: Dana Anspach, BS Certified Financial Planner | Course No. 5018

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 5h 57m | 5 GB

Lecturer: Dana Anspach, BS Certified Financial Planner | Course No. 5018

Recent statistics suggest that nearly two-thirds of Americans regret not planning properly for retirement. We tend to underestimate the key factors of retirement planning: our total lifespan; the probable length of our retirement; and, perhaps most significant, how much money we’ll need to fund those years in retirement. In fact, retirement planning can feel so overwhelming that many of us put off thinking about it at all until it’s too late to make the necessary changes.

Of course, the future tends to get here before we know it—and it does not arrive with its own financial security unless we plan it that way. In How to Plan for the Perfect Retirement, Professor Dana Anspach of Sensible Money, LLC will be your step-by-step guide to help you create the future you want. No matter how old you are or how far along in your working life, it’s never too early or too late to develop a plan that works for you. Professor Anspach will take the mystery out of retirement planning by identifying specific questions you need to ask yourself, explaining exactly how to examine your personal finances, and demonstrating how a small change now can benefit you greatly later on. With vibrant and informative graphics, illuminating statistics, revealing real-world stories, and crystal-clear explanations, this course will make planning for retirement clearer and more attainable than ever before.

What Is Retirement Planning?

According to the Federal Reserve, almost 25 percent of us have no pension or retirement savings at all. And many of those who do save money believe that is retirement planning, especially if they’re contributing to a 401(k) or IRA. But as you’ll learn from Professor Anspach, building a retirement nest egg is not the same as creating a comprehensive financial plan for your retirement years.

As she walks you through the planning process, you’ll learn that while the “accumulation” phase is not necessarily complicated, the “decumulation” phase involves more complex interactions between many moving parts. These include investments, insurance, pensions, taxes, and the need to manage numerous risks and unknowns. That complexity is the reason you need a personalized financial model—because no one can determine how much money you’ll need in retirement without analyzing your specific lifestyle, expectations, and complete financial situation.

In this course, you’ll learn 10 specific questions to ask yourself about your financial situation, the answers to which will guide you in all your retirement decisions. In addition, you will learn:

How to best plan for significant unknowns such as the future pattern of good and poor market returns, inflation, and family emergencies;

Guidelines for paying down debt versus investing during the accumulation years;

How to decide whether to rent or buy a home;

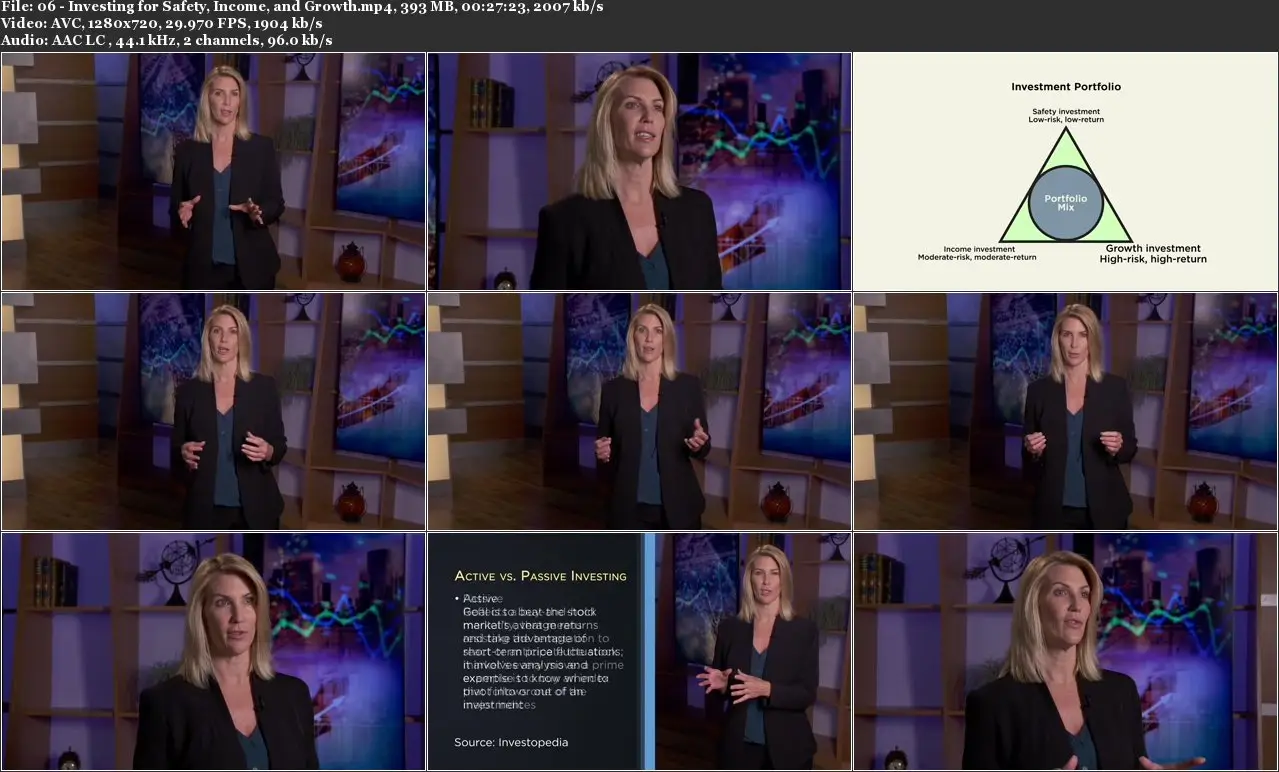

The difference between active and passive investing, and much more.

You will also learn why Professor Anspach favors a work/retirement approach she calls “a life well-worked,” which could involve working at a job you love well into your 70s. This is in opposition to the recently popularized movement called FIRE (Financial Independence, Retire Early), which involves working extremely hard in your early years, saving as much as you can, and retiring as early as possible.

Anyone Can Start Planning for Retirement—Now

Millions of Americans feel themselves limited in their options for retirement planning. But despite your personal circumstances, this course will help you personalize a plan based on your very specific needs and resources.

As Professor Anspach explains, there are specific steps you should take right now to help you plan for the future—no matter your income level, age, or family circumstance. They include:

Picture Your Future Self. Numerous studies have shown that people don’t plan for the future because they can’t picture themselves in the future. Those same studies have shown that when individuals use an app to create a virtual image of their future self, they do save more money. Now that future self is someone they “know,” and no longer just an abstract concept.

Track Your Spending. You probably know your income, but chances are you do not know what you spend. Tracking every penny of your spending for a period of time might reveal where you can find money to save now. If not, this exercise is still helpful to start identifying how much money you’ll need in order to maintain your current lifestyle in retirement.

Meet with a Retirement Planning Professional. In Dr. Anspach’s experience, meeting with a retirement professional lifts an enormous load off the shoulders of clients. Turning the vast unknown into a concrete plan allows you to take actionable steps and leave the worry behind. You’re no longer a procrastinator; you’re a proactive planner. And that feels good to everyone.

Retirement Plans in Action

You probably know many people who are retired right now. Based on their activities, travel, and overall lifestyle habits, you might think you have a picture of their financial security—but you don’t. It’s always the numbers that tell the real story—the numbers we would never ask our friends to share.

But in How to Plan for the Perfect Retirement, you will see behind the curtain. You’ll learn about financial planning for retirement by meeting:

Gabe and Mary. In their story, you’ll learn about Medicare, Social Security, deferred-income annuities, tax planning, and more. In order to meet their goal of early retirement, they had to make some important choices and adjustments, and you’ll see how they did eventually manage to build a solid financial plan that will allow them to retire with financial security, even if it wasn’t their original plan.

Sara and Jim. Jim had wanted to provide for Sara after his death and to pass money on to his children from a previous marriage. Learning from Jim’s mistakes, you’ll see why decisions made during retirement planning need to be considered individually and within the context of the larger family.

John. When John’s wife passed away during their early retirement, John needed to make changes in his financial plans. From his journey, you’ll learn about purchasing a home during retirement, home equity lines of credit, and ways to finance a move to a continuing-care retirement community.

As you watch these individuals make the many decisions that will determine their financial future, you’ll understand why Professor Anspach says, “No retiree who makes a mathematically sound withdrawal plan—and sticks with it, making necessary adjustments along the way—should ever run out of money.” With the vital information and real-world tools provided in How to Plan for the Perfect Retirement, you can take an active role in planning for your future and create a more secure and less stressful post-work life.

What Is Retirement Planning?

According to the Federal Reserve, almost 25 percent of us have no pension or retirement savings at all. And many of those who do save money believe that is retirement planning, especially if they’re contributing to a 401(k) or IRA. But as you’ll learn from Professor Anspach, building a retirement nest egg is not the same as creating a comprehensive financial plan for your retirement years.

As she walks you through the planning process, you’ll learn that while the “accumulation” phase is not necessarily complicated, the “decumulation” phase involves more complex interactions between many moving parts. These include investments, insurance, pensions, taxes, and the need to manage numerous risks and unknowns. That complexity is the reason you need a personalized financial model—because no one can determine how much money you’ll need in retirement without analyzing your specific lifestyle, expectations, and complete financial situation.

In this course, you’ll learn 10 specific questions to ask yourself about your financial situation, the answers to which will guide you in all your retirement decisions. In addition, you will learn:

How to best plan for significant unknowns such as the future pattern of good and poor market returns, inflation, and family emergencies;

Guidelines for paying down debt versus investing during the accumulation years;

How to decide whether to rent or buy a home;

The difference between active and passive investing, and much more.

You will also learn why Professor Anspach favors a work/retirement approach she calls “a life well-worked,” which could involve working at a job you love well into your 70s. This is in opposition to the recently popularized movement called FIRE (Financial Independence, Retire Early), which involves working extremely hard in your early years, saving as much as you can, and retiring as early as possible.

Anyone Can Start Planning for Retirement—Now

Millions of Americans feel themselves limited in their options for retirement planning. But despite your personal circumstances, this course will help you personalize a plan based on your very specific needs and resources.

As Professor Anspach explains, there are specific steps you should take right now to help you plan for the future—no matter your income level, age, or family circumstance. They include:

Picture Your Future Self. Numerous studies have shown that people don’t plan for the future because they can’t picture themselves in the future. Those same studies have shown that when individuals use an app to create a virtual image of their future self, they do save more money. Now that future self is someone they “know,” and no longer just an abstract concept.

Track Your Spending. You probably know your income, but chances are you do not know what you spend. Tracking every penny of your spending for a period of time might reveal where you can find money to save now. If not, this exercise is still helpful to start identifying how much money you’ll need in order to maintain your current lifestyle in retirement.

Meet with a Retirement Planning Professional. In Dr. Anspach’s experience, meeting with a retirement professional lifts an enormous load off the shoulders of clients. Turning the vast unknown into a concrete plan allows you to take actionable steps and leave the worry behind. You’re no longer a procrastinator; you’re a proactive planner. And that feels good to everyone.

Retirement Plans in Action

You probably know many people who are retired right now. Based on their activities, travel, and overall lifestyle habits, you might think you have a picture of their financial security—but you don’t. It’s always the numbers that tell the real story—the numbers we would never ask our friends to share.

But in How to Plan for the Perfect Retirement, you will see behind the curtain. You’ll learn about financial planning for retirement by meeting:

Gabe and Mary. In their story, you’ll learn about Medicare, Social Security, deferred-income annuities, tax planning, and more. In order to meet their goal of early retirement, they had to make some important choices and adjustments, and you’ll see how they did eventually manage to build a solid financial plan that will allow them to retire with financial security, even if it wasn’t their original plan.

Sara and Jim. Jim had wanted to provide for Sara after his death and to pass money on to his children from a previous marriage. Learning from Jim’s mistakes, you’ll see why decisions made during retirement planning need to be considered individually and within the context of the larger family.

John. When John’s wife passed away during their early retirement, John needed to make changes in his financial plans. From his journey, you’ll learn about purchasing a home during retirement, home equity lines of credit, and ways to finance a move to a continuing-care retirement community.

As you watch these individuals make the many decisions that will determine their financial future, you’ll understand why Professor Anspach says, “No retiree who makes a mathematically sound withdrawal plan—and sticks with it, making necessary adjustments along the way—should ever run out of money.” With the vital information and real-world tools provided in How to Plan for the Perfect Retirement, you can take an active role in planning for your future and create a more secure and less stressful post-work life.

TTC Video - How to Plan for the Perfect Retirement