Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance

WEBRip | English | MP4 | 960 x 540 | AVC ~63.8 kbps | 25 fps

AAC | 128 Kbps | 48.0 KHz | 2 channels | ~8 hours | 5.98 GB

Genre: eLearning Video / Maths, Economics & Finance

WEBRip | English | MP4 | 960 x 540 | AVC ~63.8 kbps | 25 fps

AAC | 128 Kbps | 48.0 KHz | 2 channels | ~8 hours | 5.98 GB

Genre: eLearning Video / Maths, Economics & Finance

Mathematical Methods for Quantitative Finance covers topics from calculus and linear algebra that are fundamental for the study of mathematical finance. Students successfully completing this course will be mathematically well prepared to study quantitative finance at the graduate level.The Mathematical Methods for Quantitative Finance course reviews the mathematical methods fundamental for the study of quantitative and computational finance. The areas of focus include calculus and multivariable calculus, constrained and unconstrained optimization, and linear algebra.

Topics covered include the following:

Functions and inverse functions

Limits, derivatives, partial derivatives, and chain rule

Integrals and multiple integrals, changing the order of differentiation and integration

Taylor series approximations

Newton’s method

Lagrange multiplier method

Vector and matrix arithmetic, determinants, eigenvalue-eigenvector decomposition, singular value decomposition

Numerical methods for optimization

Course goal:

Upon completion of the course students will know the fundamental mathematical concepts needed to effectively study quantitative finance areas such as fixed income, options and derivatives, portfolio optimization, and quantitative risk management.

Course Objectives:

Upon completion of the course students will:

Understand the concept of a limit, differentiation, and integration;

Be able to compute partial derivatives and multiple integrals;

Understand the utility of matrix decompositions;

Be able to use Lagrange multipliers to solve constrained optimization problems; and

Apply the above methods to problems arising in finance.

also You can watch my other helpful: Coursera-posts

(if old file-links don't show activity, try copy-paste them to the address bar)

General

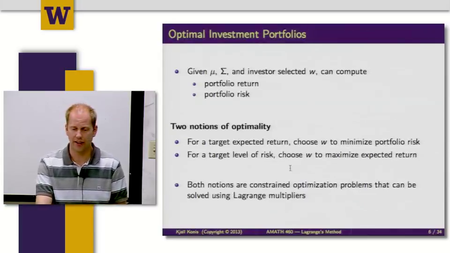

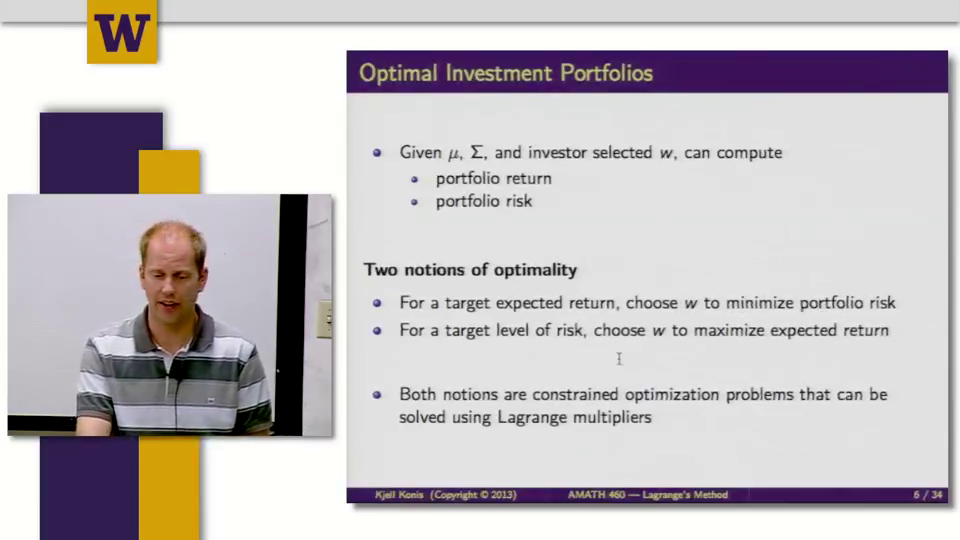

Complete name : Mathematical Methods for Quantitative Finance 8.1 W7.1.1 – Optimal Investment Portfolios (1732).mp4

Format : MPEG-4

Format profile : Base Media

Codec ID : isom

File size : 24.8 MiB

Duration : 17mn 32s

Overall bit rate mode : Variable

Overall bit rate : 198 Kbps

Movie name : MMfQF_W7_P1_Kjell_OptimalInvestmentPortfolios_FINAL

Composer : Jon Keib

Writing application : Lavf52.99.1

desc : This video is about MMfQF_W7_P1_Kjell_OptimalInvestmentPortfolios

Video

ID : 1

Format : AVC

Format/Info : Advanced Video Codec

Format profile : High@L3.0

Format settings, CABAC : Yes

Format settings, ReFrames : 4 frames

Codec ID : avc1

Codec ID/Info : Advanced Video Coding

Duration : 17mn 32s

Bit rate : 63.8 Kbps

Width : 960 pixels

Height : 540 pixels

Display aspect ratio : 16:9

Frame rate mode : Constant

Frame rate : 25.000 fps

Color space : YUV

Chroma subsampling : 4:2:0

Bit depth : 8 bits

Scan type : Progressive

Bits/(Pixel*Frame) : 0.005

Stream size : 8.00 MiB (32%)

Writing library : x264 core 114 r1913 5fd3dce

Encoding settings : cabac=1 / ref=1 / deblock=1:0:0 / analyse=0x3:0x113 / me=hex / subme=2 / psy=1 / psy_rd=0.00:0.00 / mixed_ref=0 / me_range=16 / chroma_me=1 / trellis=0 / 8x8dct=1 / cqm=0 / deadzone=21,11 / fast_pskip=1 / chroma_qp_offset=0 / threads=3 / sliced_threads=0 / nr=0 / decimate=1 / interlaced=0 / constrained_intra=0 / bframes=3 / b_pyramid=2 / b_adapt=1 / b_bias=0 / direct=1 / weightb=1 / open_gop=0 / weightp=0 / keyint=250 / keyint_min=25 / scenecut=40 / intra_refresh=0 / rc_lookahead=10 / rc=crf / mbtree=1 / crf=28.0 / qcomp=0.60 / qpmin=0 / qpmax=69 / qpstep=4 / ip_ratio=1.41 / aq=1:1.00

Language : English

Audio

ID : 2

Format : AAC

Format/Info : Advanced Audio Codec

Format profile : LC

Codec ID : 40

Duration : 17mn 32s

Bit rate mode : Variable

Bit rate : 128 Kbps

Channel(s) : 2 channels

Channel positions : Front: L R

Sampling rate : 48.0 KHz

Compression mode : Lossy

Delay relative to video : -2ms

Stream size : 16.0 MiB (65%)

Language : English

Complete name : Mathematical Methods for Quantitative Finance 8.1 W7.1.1 – Optimal Investment Portfolios (1732).mp4

Format : MPEG-4

Format profile : Base Media

Codec ID : isom

File size : 24.8 MiB

Duration : 17mn 32s

Overall bit rate mode : Variable

Overall bit rate : 198 Kbps

Movie name : MMfQF_W7_P1_Kjell_OptimalInvestmentPortfolios_FINAL

Composer : Jon Keib

Writing application : Lavf52.99.1

desc : This video is about MMfQF_W7_P1_Kjell_OptimalInvestmentPortfolios

Video

ID : 1

Format : AVC

Format/Info : Advanced Video Codec

Format profile : High@L3.0

Format settings, CABAC : Yes

Format settings, ReFrames : 4 frames

Codec ID : avc1

Codec ID/Info : Advanced Video Coding

Duration : 17mn 32s

Bit rate : 63.8 Kbps

Width : 960 pixels

Height : 540 pixels

Display aspect ratio : 16:9

Frame rate mode : Constant

Frame rate : 25.000 fps

Color space : YUV

Chroma subsampling : 4:2:0

Bit depth : 8 bits

Scan type : Progressive

Bits/(Pixel*Frame) : 0.005

Stream size : 8.00 MiB (32%)

Writing library : x264 core 114 r1913 5fd3dce

Encoding settings : cabac=1 / ref=1 / deblock=1:0:0 / analyse=0x3:0x113 / me=hex / subme=2 / psy=1 / psy_rd=0.00:0.00 / mixed_ref=0 / me_range=16 / chroma_me=1 / trellis=0 / 8x8dct=1 / cqm=0 / deadzone=21,11 / fast_pskip=1 / chroma_qp_offset=0 / threads=3 / sliced_threads=0 / nr=0 / decimate=1 / interlaced=0 / constrained_intra=0 / bframes=3 / b_pyramid=2 / b_adapt=1 / b_bias=0 / direct=1 / weightb=1 / open_gop=0 / weightp=0 / keyint=250 / keyint_min=25 / scenecut=40 / intra_refresh=0 / rc_lookahead=10 / rc=crf / mbtree=1 / crf=28.0 / qcomp=0.60 / qpmin=0 / qpmax=69 / qpstep=4 / ip_ratio=1.41 / aq=1:1.00

Language : English

Audio

ID : 2

Format : AAC

Format/Info : Advanced Audio Codec

Format profile : LC

Codec ID : 40

Duration : 17mn 32s

Bit rate mode : Variable

Bit rate : 128 Kbps

Channel(s) : 2 channels

Channel positions : Front: L R

Sampling rate : 48.0 KHz

Compression mode : Lossy

Delay relative to video : -2ms

Stream size : 16.0 MiB (65%)

Language : English

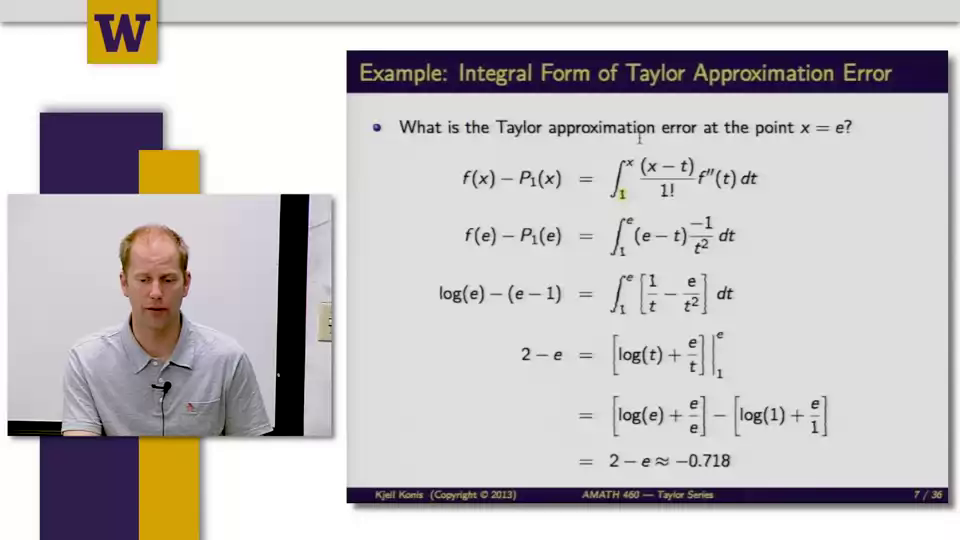

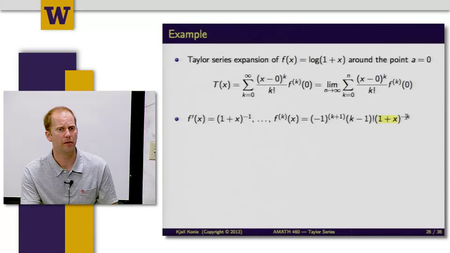

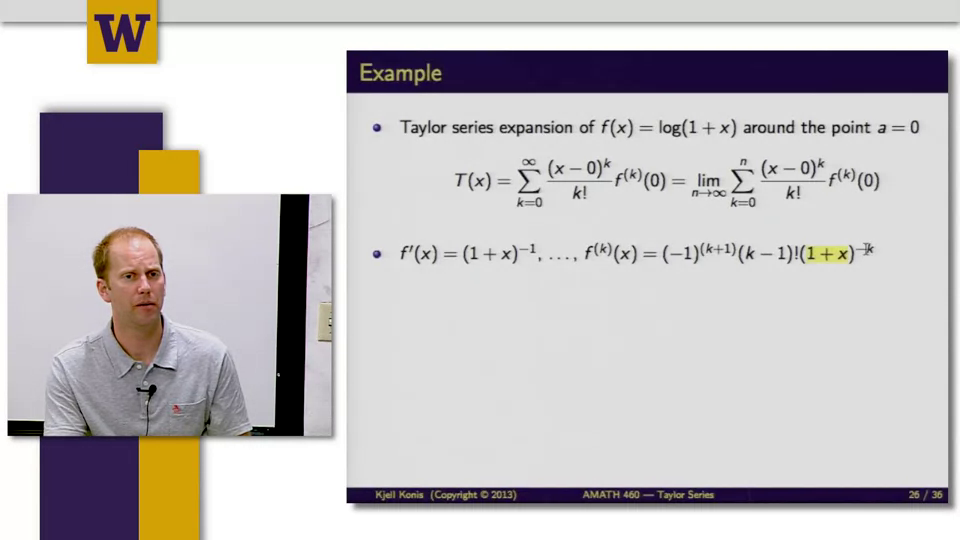

Screenshots

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)

✅ Exclusive eLearning Videos ParRus-blog ← add to bookmarks

Feel free to contact me PM

when links are dead or want any repost

Feel free to contact me PM

when links are dead or want any repost

Coursera - Mathematical Methods for Quantitative Finance (University of Washington)