Financial Engineering and Artificial Intelligence in Python

Financial Engineering and Artificial Intelligence in Python

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 20h 3m | 6.09 GB

Created by Lazy Programmer Team

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 20h 3m | 6.09 GB

Created by Lazy Programmer Team

Financial Analysis, Time Series Analysis, Portfolio Optimization, CAPM, Algorithmic Trading, Q-Learning, and MORE!

What you'll learn

Forecasting stock prices and stock returns

Time series analysis

Holt-Winters exponential smoothing model

ARIMA

Efficient Market Hypothesis

Random Walk Hypothesis

Exploratory data analysis

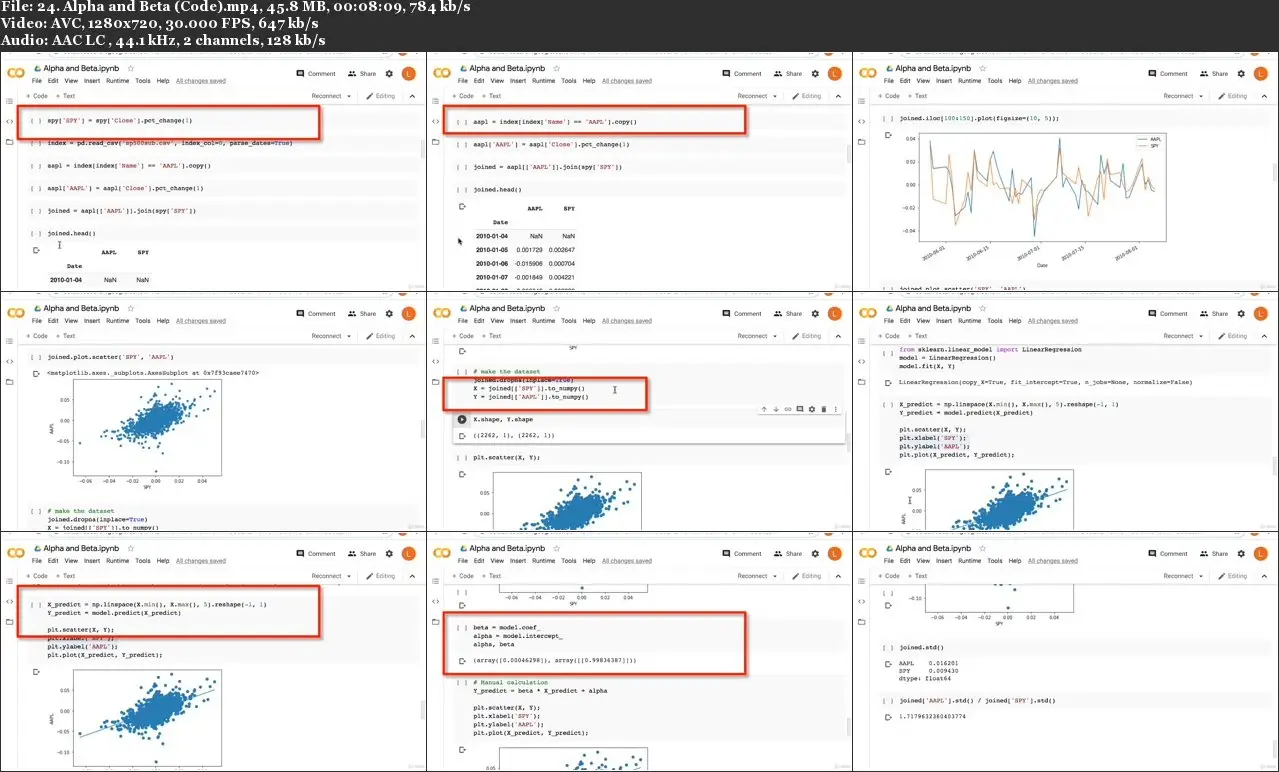

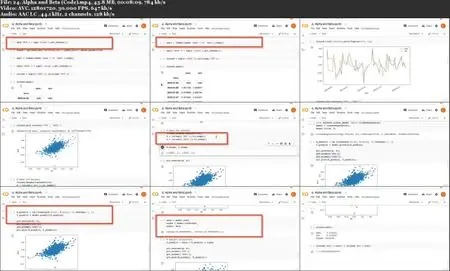

Alpha and Beta

Distributions and correlations of stock returns

Modern portfolio theory

Mean-Variance Optimization

Efficient frontier, Sharpe ratio, Tangency portfolio

CAPM (Capital Asset Pricing Model)

Q-Learning for Algorithmic Trading

Requirements

Decent Python coding skills

Numpy, Matplotlib, Pandas, and Scipy (I teach this for free! My gift to the community)

Matrix arithmetic

Probability

Description

Have you ever thought about what would happen if you combined the power of machine learning and artificial intelligence with financial engineering?

Today, you can stop imagining, and start doing.

This course will teach you the core fundamentals of financial engineering, with a machine learning twist.

We will cover must-know topics in financial engineering, such as:

Exploratory data analysis, significance testing, correlations, alpha and beta

Time series analysis, simple moving average, exponentially-weighted moving average

Holt-Winters exponential smoothing model

ARIMA and SARIMA

Efficient Market Hypothesis

Random Walk Hypothesis

Time series forecasting ("stock price prediction")

Modern portfolio theory

Efficient frontier / Markowitz bullet

Mean-variance optimization

Maximizing the Sharpe ratio

Convex optimization with Linear Programming and Quadratic Programming

Capital Asset Pricing Model (CAPM)

Algorithmic trading

Statistical Factor Models

Regime Detection with Hidden Markov Models

In addition, we will look at various non-traditional techniques which stem purely from the field of machine learning and artificial intelligence, such as:

Regression models

Classification models

Unsupervised learning

Reinforcement learning and Q-learning

Algorithmic trading (trend-following, machine learning, and Q-learning-based strategies)

Statistical factor models

Regime detection and modeling volatility clustering with HMMs

We will learn about the greatest flub made in the past decade by marketers posing as "machine learning experts" who promise to teach unsuspecting students how to "predict stock prices with LSTMs". You will learn exactly why their methodology is fundamentally flawed and why their results are complete nonsense. It is a lesson in how not to apply AI in finance.

As the author of ~30 courses in machine learning, deep learning, data science, and artificial intelligence, I couldn't help but wander into the vast and complex world of financial engineering.

This course is for anyone who loves finance or artificial intelligence, and especially if you love both!

Whether you are a student, a professional, or someone who wants to advance their career - this course is for you.

Thanks for reading, I will see you in class!

Suggested Prerequisites:

Matrix arithmetic

Probability

Decent Python coding skills

Numpy, Matplotlib, Scipy, and Pandas (I teach this for free, no excuses!)

Who this course is for:

Anyone who loves or wants to learn about financial engineering

Students and professionals who want to advance their career in finance or artificial intelligence and machine learning

Financial Engineering and Artificial Intelligence in Python