Excelbusinesstools.com Portfolio Optimization for Excel Datecode 20210120

Excelbusinesstools.com Portfolio Optimization for Excel Datecode 20210120 | 0.7 Mb

The Excel Portfolio Optimization Template establishes optimal capital weightings for portfolios of financial investments or business assets to maximize return and minimize drawdown risk. Risk assessment options and portfolio dynamics can be adjusted to analyze optimization on portfolios based on specific business requirements, extrapolations and preferences. Portfolio management is assisted with technical analysis including indicator parameter optimization with back tested total returns in order to establish optimal trading strategies at individual investment and portfolio levels.

Key features of the Excel Portfolio Optimization template include:

A simple and logical data input and work flow is provided with adaptable options accompanied by integrated help information.

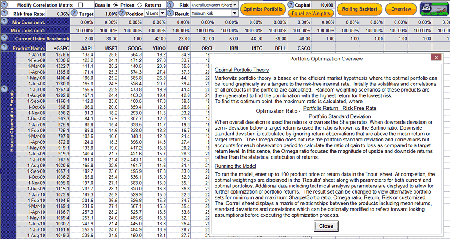

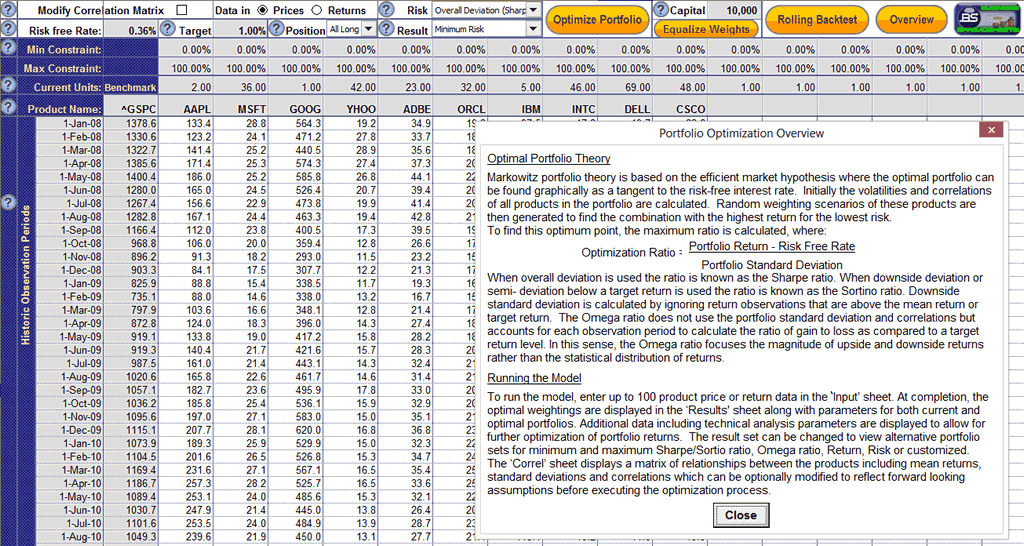

The input accommodates for up to 100 securities or business cash flow data from which current portfolio weightings, returns and risk correlations are calculated. Historical prices for financial security data can be freely downloaded from the internet with the accompanying market data download solution.

The market data solution to download financial security price data also provides detailed return analysis and statistics to compare two securities or securities with benchmark indices. A valuation option compares a discounted cash flow valuation of market securities based on consensus analyst earnings expectations to determine whether stocks are under or overvalued by comparing with market capitalization.

Minimum and maximum weighting constraints can be specified for each asset for the optimized portfolio to reflect obligations and capital allocation restrictions.

The correlation matrix and portfolio dynamics calculated from the input data can be modified before running the optimization process. This allows for assumptions on future trends and relationships to be accounted for in the optimal portfolio.

Portfolio risk for optimization can be based on overall volatility under the Sharpe ratio or downside risk or semi-deviation below a target return under Sortino ratio.

Optimization can be made on the Sharpe or Sortino ratio as well as return, risk and the Omega ratio which analyzes the proportion of upside to downside return magnitude. Results are saved for both minimum and maximum levels so that resulting portfolios can be loaded and viewed without requiring additional optimization processes.

Additional options allow for flexibility and customization of analysis such as calculating quantities to apply a nominal capital amount equally to investments and exporting results to a standalone files.

Existing and optimized portfolios can be specified with both Long and Short positions as either all long, all short or long/short mixed whereby the optimal mix of long and short positions is identified.

The comparison between the current and optimized portfolio is displayed graphically as well as unit buy and sell quantities required for each investment in the portfolio.

A target return matching the input periodicity can be specified for which the probability of achieving is calculated and displayed using Monte Carlo simulation.

The rolling back test function allows the specification of periodic optimizations within the historical time period to analyze the subsequent effects of the optimizations on the portfolio performance.

Technical analysis with Buy and Sell signals and back tested total return gain is performed for the overall portfolio and each investment. Configurable technical analysis indicators include: Simple Moving Average (SMA), Rate of Change (ROC), Moving Average Convergence/Divergence (MACD), Relative Strength Index (RSI) and Bollinger Bands.

Automatic optimization of technical indicator period constants find the parameters that maximize back tested return at both individual investment and overall portfolio levels.

Technical analysis results show the comparison of back tested total returns between no action and signal trading for the total portfolio, current and optimal portfolio as indices as well as the individual investments. These results can be used in conjunction with last observation indicator screening flags and signals to establish optimal trading strategies for the portfolio.

Requirements

- Excel 97-2016

- Excel 2004, 2011 or 2016

Home Page - http://www.business-spreadsheets.com/portopt.htm